Know Portfolio RISK –

Evaluate Manager SKILL

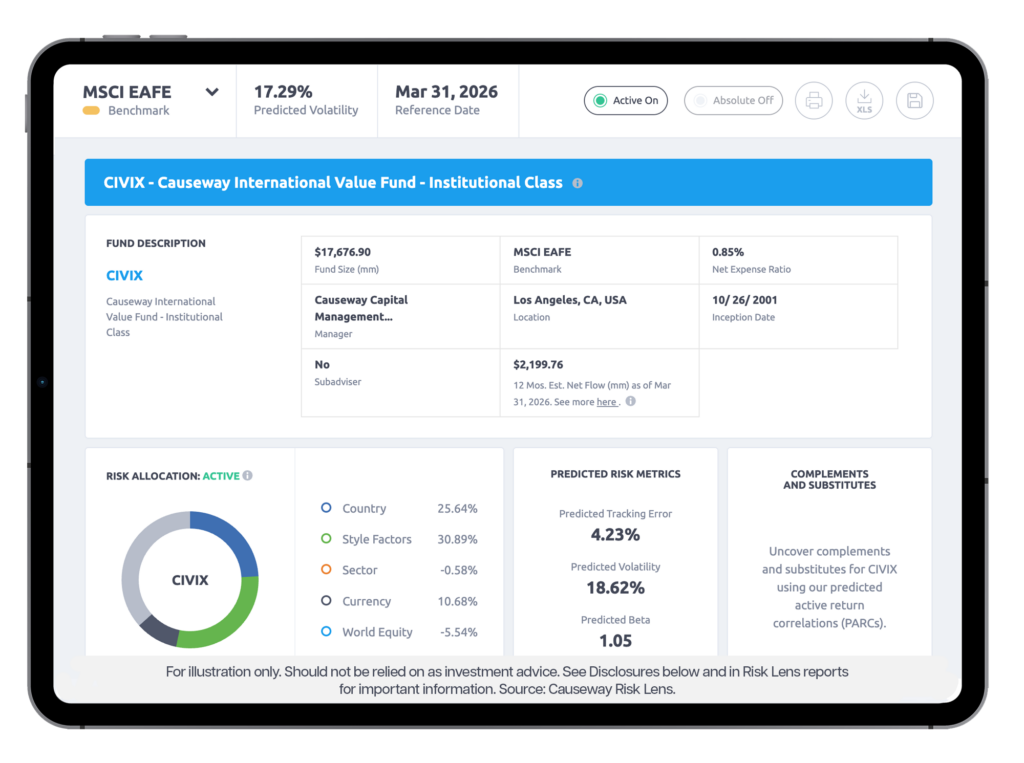

Risk

Skill

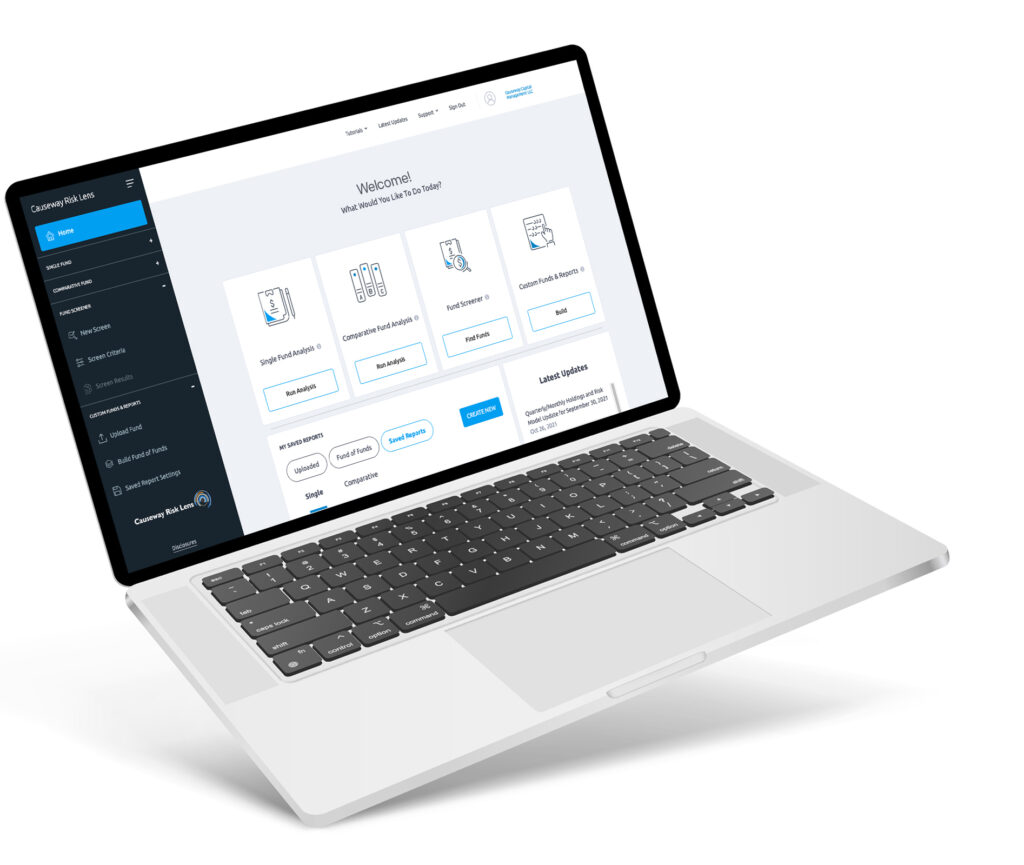

Fund Screener

Fund Screener screens RISK and SKILL metrics

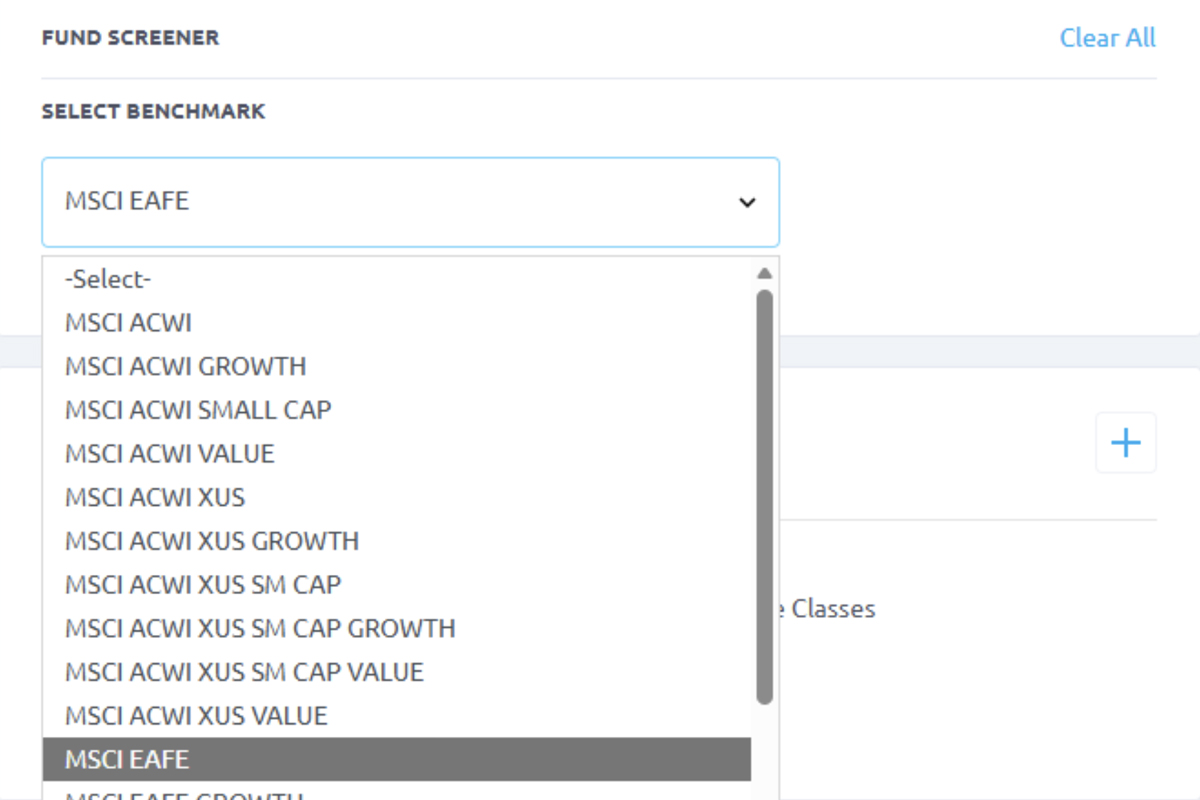

Pick A Benchmark –

Choose from 37 benchmarks across all major geographies

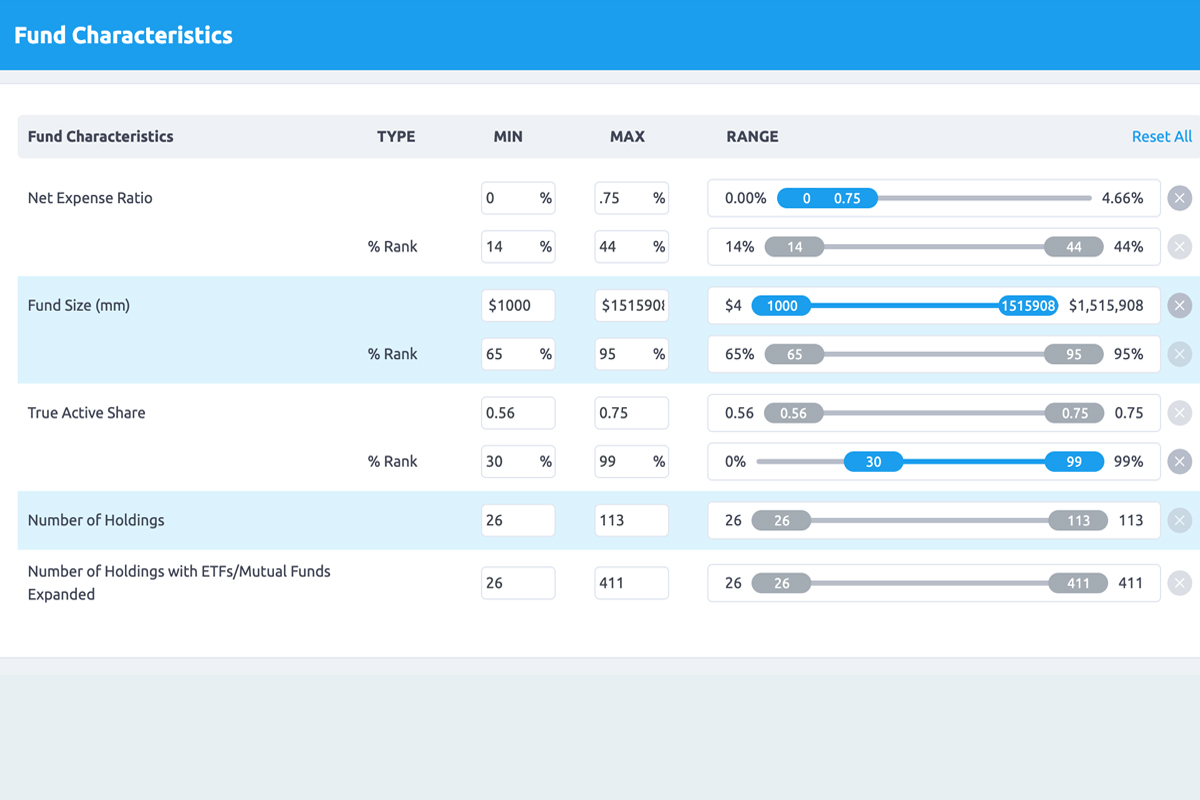

Select Your Screens –

Filter on both risk exposures and skill metrics

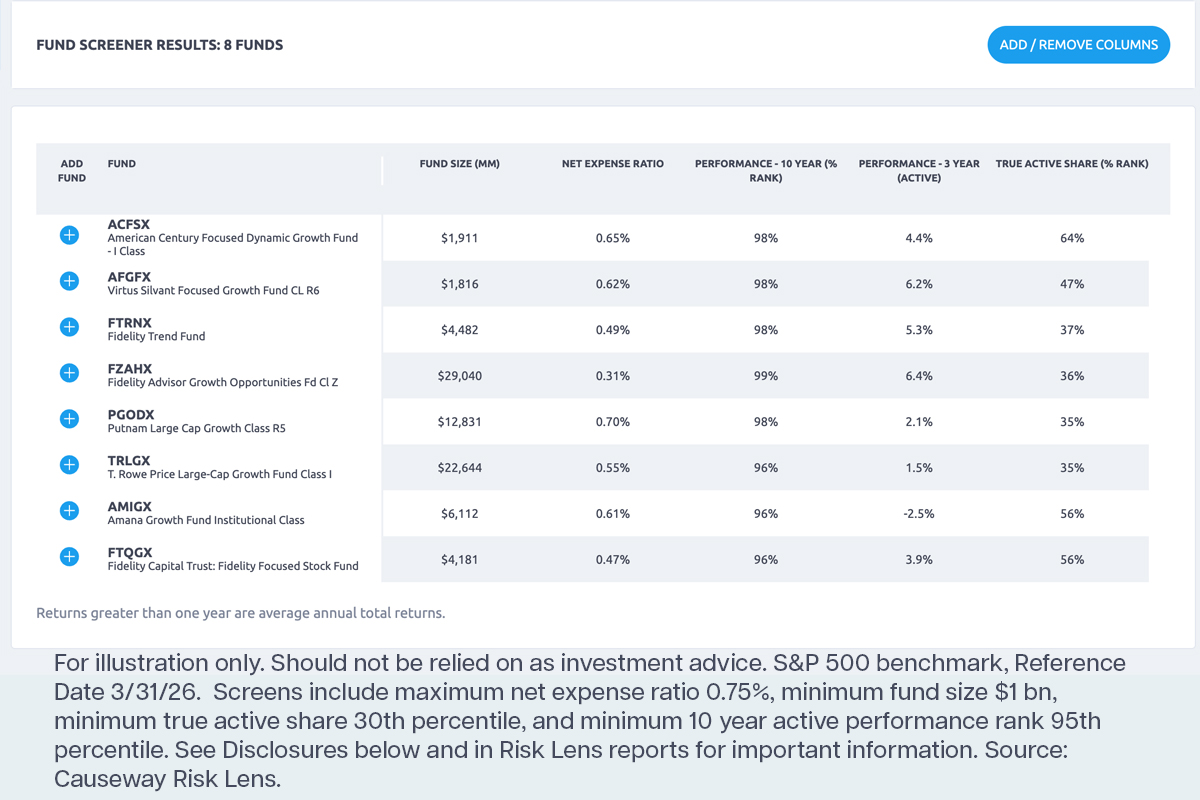

Find Your Funds –

Find managers that meet your criteria

Why Risk Lens?

RISK

Holdings-based – we estimate predicted risks and correlations using the latest available public fund holdings. Many other tools are returns-based, only showing past risk metrics.

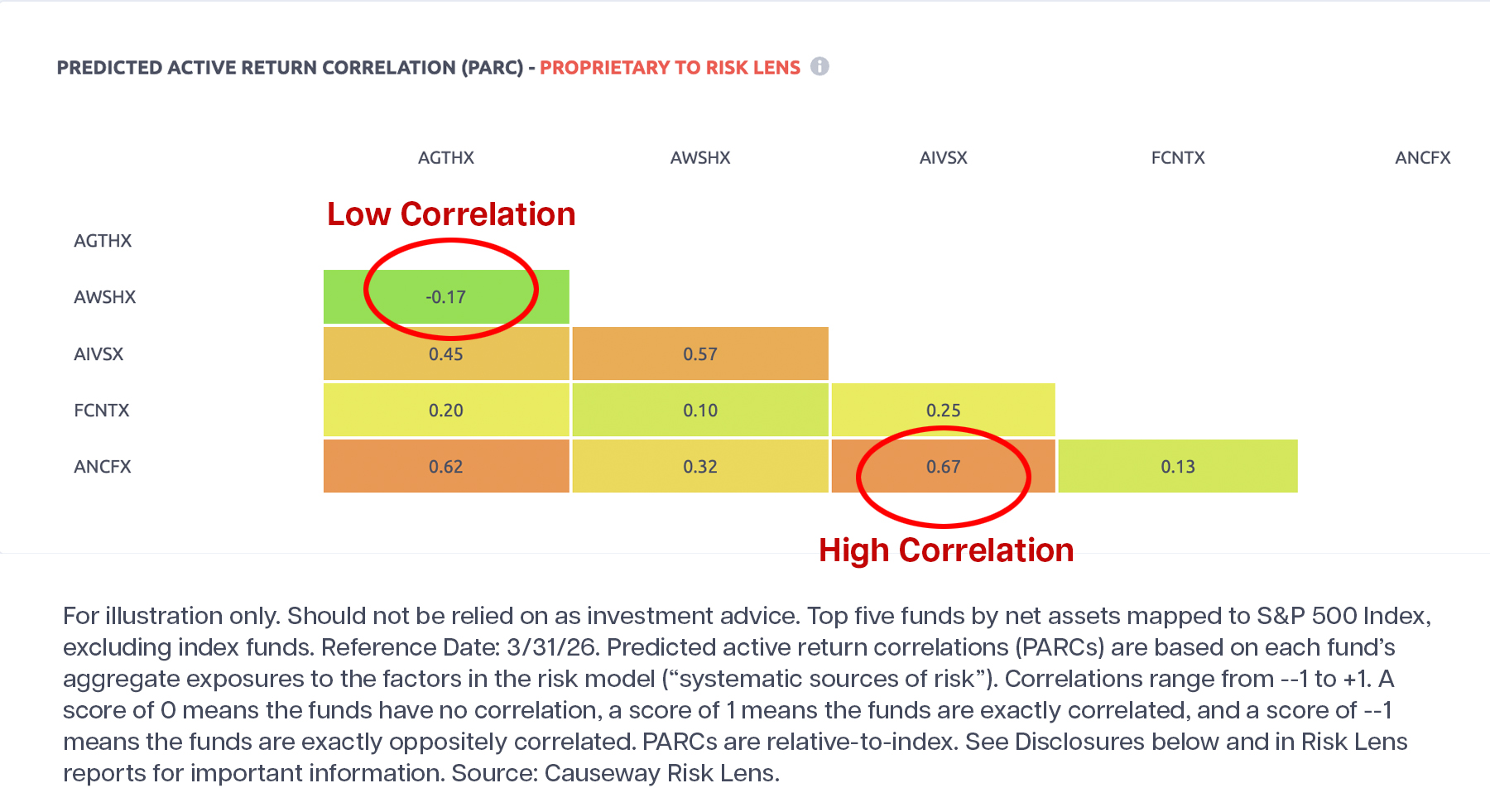

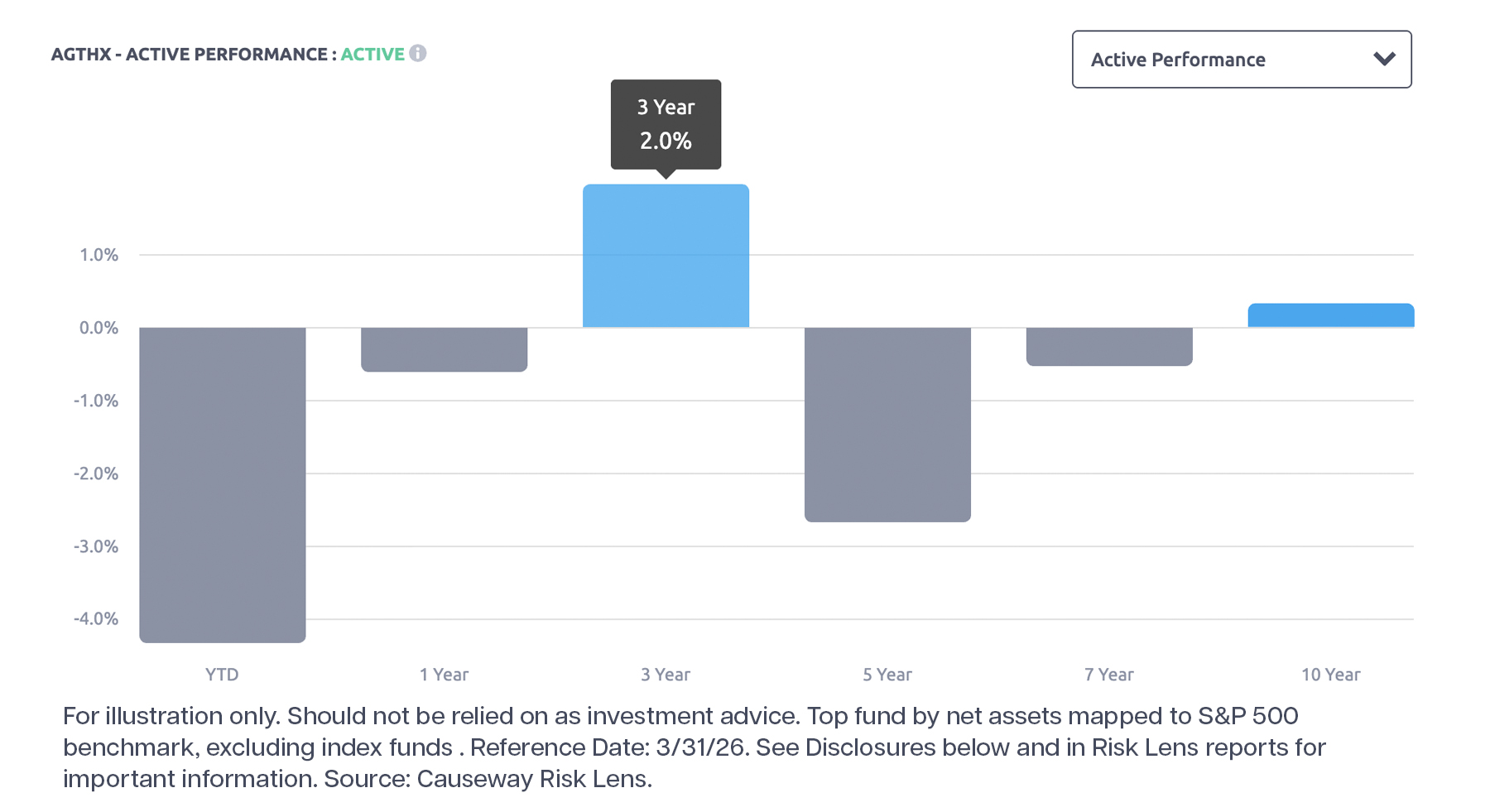

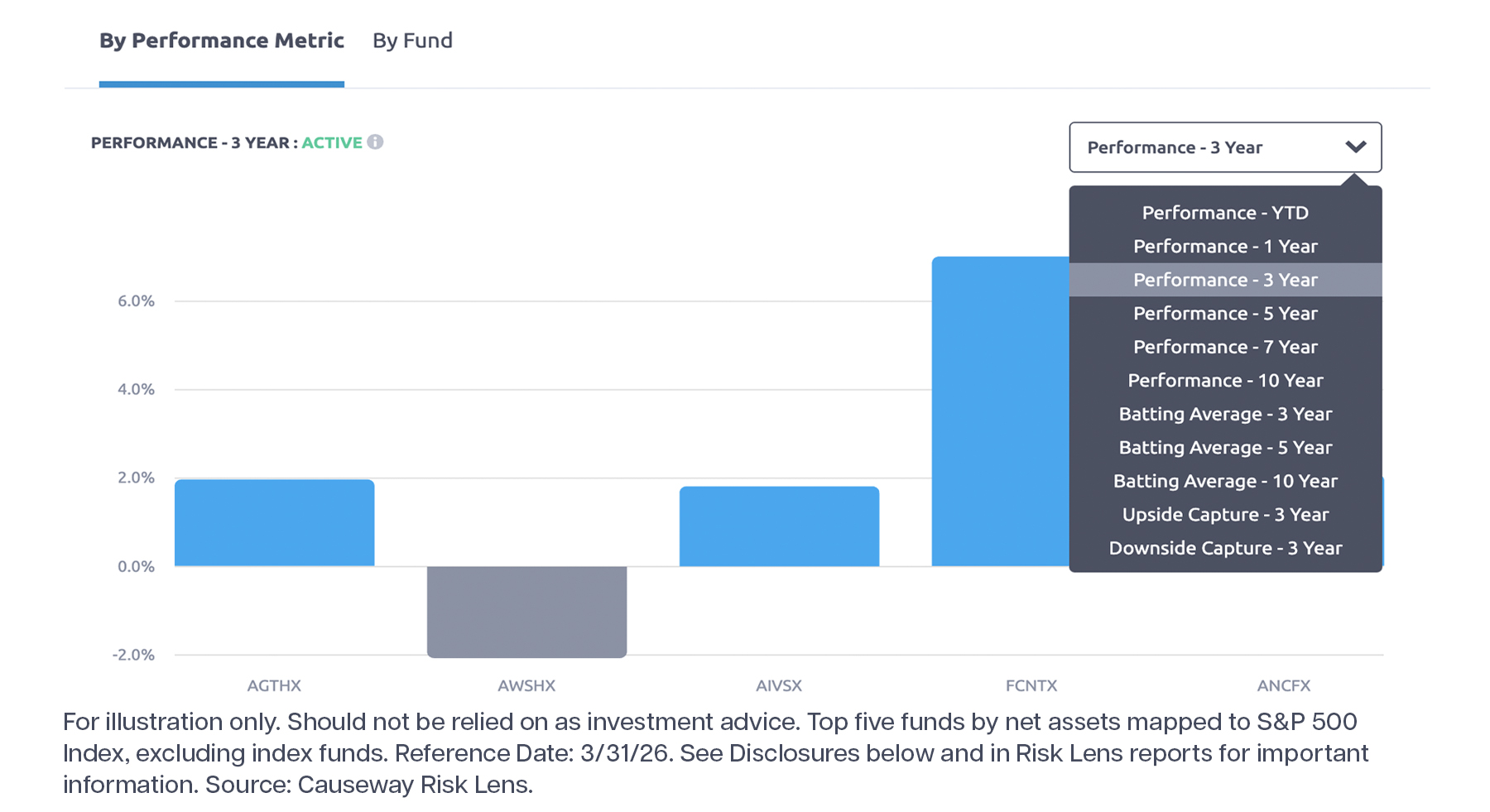

SKILL

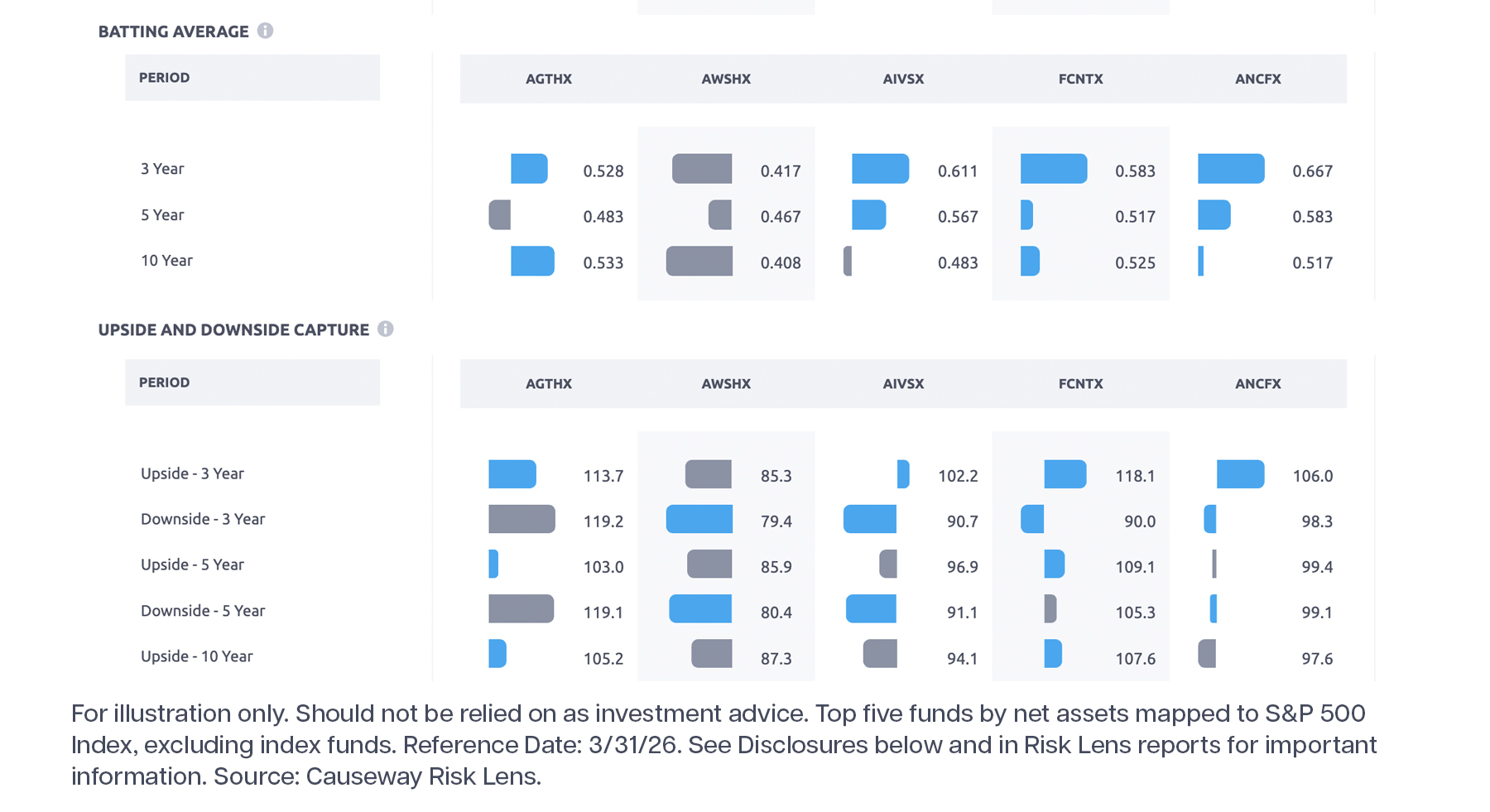

Performance Report compares past active performance, batting averages, upside/downside capture, and other skill metrics.

FUND SCREENER

Screens managers on RISK and SKILL metrics.

FREE

Access the power of Risk Lens at no cost.

Client testimonials

What’s New

Risk Metrics that Matter, May 2026

Risk Lens: Is Your Manager Phoning It In?, March 2026

Who Beat The S&P 500 Index?, November 2025

Donuts Are Good For You: Q&A with Portfolio Manager Joe Gubler, August 2025

Best Performing US Large Cap Growth Funds At June 30, July 2025